How I Learned to Invest in My Hearing — And Why It Changed Everything

What if the smartest investment you ever made wasn’t in stocks or real estate, but in yourself? I didn’t think twice about my hearing until it started slipping — and suddenly, everything changed. From missing key conversations to feeling isolated, I realized hearing aids weren’t just medical devices; they were life-changing tools. This is the story of how shifting my mindset turned a personal health decision into one of the most rewarding investments I’ve ever made. It’s not about quick returns or flashy gains. It’s about preserving connection, clarity, and capability — the quiet but powerful foundations of a full, productive life. What began as a reluctant visit to an audiologist became a lesson in long-term thinking, self-worth, and financial wisdom.

The Moment I Realized My Hearing Was Fading

I’ll never forget the first time I asked someone to repeat themselves — not once, but three times — during a simple dinner chat. It wasn’t just awkward; it was alarming. I was in my early fifties, surrounded by family, and yet I kept missing punchlines, mishearing names, and nodding along to conversations I barely followed. At first, I blamed the background music or assumed I was just tired. But the pattern grew harder to ignore. Phone calls became stressful. I’d hang up confused, replaying what I thought I’d heard. In meetings, I caught myself watching lips more than listening, filling in gaps with guesses. The strain was constant, like trying to read a book in dim light — possible, but exhausting.

The emotional toll was just as real. I started avoiding gatherings, making excuses to skip group dinners or family events. I didn’t want to be the person who constantly said, “What?” or laughed at the wrong moment. I felt disconnected, even when I was physically present. What I didn’t realize then was that I wasn’t alone. According to the National Institute on Deafness and Other Communication Disorders, approximately 15% of American adults report some trouble hearing. Among those over 60, the number rises significantly. Yet studies show that people wait an average of seven years from the time they notice hearing loss to the time they seek help. That delay isn’t just about cost — it’s about perception. Many see hearing loss as an inevitable part of aging, not a treatable condition.

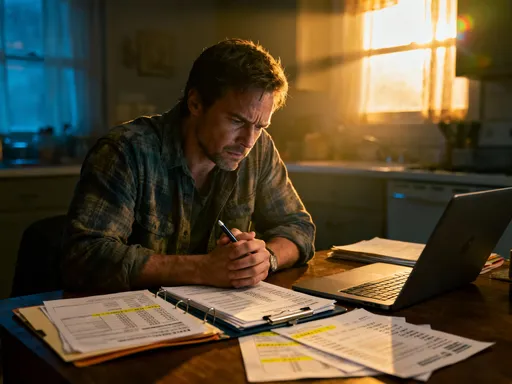

For me, the turning point came during a work presentation. I misheard a key instruction and delivered the wrong data. It wasn’t a major error, but it shook my confidence. I realized that if I couldn’t trust my own ears in a professional setting, I was putting my career at risk. That night, I searched online for local hearing clinics and made an appointment. Walking into the office felt like admitting defeat, but it was actually the first step toward regaining control. The audiologist explained that my hearing loss was mild to moderate, primarily in the higher frequencies — a common pattern associated with aging and noise exposure. The good news: it was manageable. The better news: treatment could improve not just my hearing, but my quality of life. But the next question loomed large — could I afford it?

Reframing Hearing Aids: From Cost to Investment

When I first saw the price tag — $3,000 to $6,000 for a pair of hearing aids — my stomach dropped. That was more than I’d spent on a vacation, a new laptop, even some home repairs. My immediate reaction was, “This is too expensive for a device I’m supposed to hide.” I walked out of the clinic that day unsure whether I could justify the expense. But something the audiologist said stayed with me: “You’re not buying a gadget. You’re buying your ability to engage with the world.” That phrase shifted something in me. I began to ask not “Can I afford hearing aids?” but “Can I afford *not* to have them?”

I started calculating the hidden costs of untreated hearing loss. At work, I was already making small mistakes — misheard emails, delayed responses, repeated questions. Over time, that could mean missed promotions or reduced responsibilities. In relationships, I was withdrawing. I wasn’t present with my children or my spouse. Emotional distance doesn’t come with a price tag, but it carries real consequences. Research from Johns Hopkins University has linked untreated hearing loss to higher risks of depression, cognitive decline, and even dementia. The financial burden of those conditions — in medical care, lost independence, and reduced quality of life — far exceeds the cost of early intervention.

I began to see hearing aids not as a medical expense, but as a long-term investment in my human capital. Like continuing education, professional training, or a reliable car for commuting, they were tools that enabled me to function at my best. A study published in the Journal of the American Academy of Audiology found that hearing aid users reported improved job performance and greater earning potential. Another analysis showed that treating hearing loss could reduce healthcare costs over time by preventing falls, hospitalizations, and other complications. When I reframed the purchase this way, the number on the invoice didn’t disappear — but it made sense. I wasn’t spending money; I was protecting my future self.

Why Your Mindset Determines Your Financial Outcome

Investing in health is different from most financial decisions. When you buy a stock, you expect a return. When you save for a car, you know exactly what you’re working toward. But health investments are intangible at first. You pay today for benefits that unfold slowly — sharper focus, better relationships, fewer doctor visits. That delay makes it easy to deprioritize. We’re wired to value immediate rewards over long-term gains, a bias behavioral economists call “present bias.” That’s why so many people skip preventive care, delay screenings, or avoid treatments until symptoms become unbearable.

My hesitation with hearing aids wasn’t just about money — it was about uncertainty. I couldn’t guarantee that they would work perfectly or that I’d adjust quickly. But I realized that the same logic applies to other smart financial habits. No one knows exactly how much their retirement fund will grow, yet people contribute consistently because they trust the process. Similarly, building an emergency fund doesn’t promise excitement — it offers security. Treating hearing loss is like paying into a personal resilience account. The returns aren’t in dollars, but in energy, confidence, and connection.

The mindset shift was crucial. I stopped asking, “Is this worth it?” and started asking, “What will it cost me to wait?” That question changed everything. I thought about how much I’d already lost — conversations, opportunities, peace of mind. I realized that waiting wouldn’t save me money; it would only increase the risk of deeper problems. A prevention-first approach isn’t about avoiding all costs — it’s about choosing which costs to pay. You can pay a little now for treatment, or pay much more later for consequences. That principle applies far beyond hearing. Regular check-ups, vision care, mental health support — all are forms of financial self-protection. Once I embraced that philosophy, the decision to move forward felt less like a burden and more like a responsibility to myself.

How Hearing Aids Pay You Back — Without Promising Returns

Let’s be clear: I can’t promise that hearing aids will make you rich. No ethical professional would. But what I *can* say is that they helped me stay sharp, engaged, and productive — all of which support financial stability. After wearing them for a few months, I noticed subtle but significant changes. At work, I stopped dreading conference calls. I could follow rapid discussions, contribute ideas, and catch nuances in tone and timing. My confidence returned. I wasn’t just hearing better — I was participating more fully. That level of engagement matters. In today’s knowledge economy, your ability to communicate clearly and think quickly is directly tied to your value.

The cognitive benefits were just as important. Before, I was constantly straining to understand speech, especially in noisy environments. That mental effort, known as “cognitive load,” left me tired by midday. I’d come home drained, with less energy for family, hobbies, or even simple decisions. Hearing aids reduced that strain. With less effort needed to process sound, my brain had more capacity for other tasks. Research from the University of Colorado has shown that untreated hearing loss forces the brain to reorganize, diverting resources from memory and attention. By supporting auditory input, hearing aids help preserve cognitive function — a benefit that pays off for years.

On a personal level, the impact was profound. I started enjoying family dinners again. I could hear my granddaughter’s jokes, my spouse’s quiet observations, the subtle humor in everyday talk. I stopped feeling like an outsider in my own home. Stronger relationships don’t appear on a balance sheet, but they contribute to emotional well-being, which in turn supports physical health and resilience. A study from the National Council on Aging found that hearing aid users reported higher levels of happiness, improved family relationships, and greater social involvement. These aren’t soft benefits — they’re foundational to a stable, fulfilling life. And when you’re emotionally stable and socially connected, you’re better equipped to make sound financial decisions, manage stress, and plan for the future.

Smart Ways to Manage the Financial Load

Even with the right mindset, the upfront cost is real. Most insurance plans still don’t cover hearing aids for adults, though that’s slowly changing. I had to be strategic. The first step was understanding what I actually needed. I learned that hearing aids come in different technology levels — basic, mid-range, and premium — with varying features like noise reduction, Bluetooth connectivity, and directional microphones. While the top models offer advanced capabilities, many people achieve excellent results with mid-tier devices. I didn’t need every feature; I needed clarity in everyday situations.

I explored financing options. Some clinics offer payment plans with low or no interest, allowing you to spread the cost over 12 to 24 months. I also looked into whether my flexible spending account (FSA) or health savings account (HSA) could be used — and yes, hearing aids are typically eligible expenses. That allowed me to use pre-tax dollars, effectively reducing the cost by 20% or more depending on my tax bracket. I also researched whether my employer offered any wellness benefits or hearing aid reimbursement programs — some do, though they’re still uncommon.

Another option I considered was refurbished or pre-owned devices. Some reputable clinics offer certified, cleaned, and tested hearing aids at a lower price. These are not used, damaged products — they’re often demo units or returns with full warranties. I also learned about manufacturer discount programs and nonprofit organizations that assist with hearing care costs for qualifying individuals. The key was doing thorough research and working with a trusted audiologist who could guide me without pushing the most expensive option. I wanted value, not just savings. I also made sure the provider offered a trial period — typically 30 to 60 days — so I could test the devices in real life before committing. That peace of mind was worth its weight in gold.

Avoiding Common Financial Traps in Healthcare Spending

The healthcare market is full of well-meaning advice — and some misleading offers. Early in my research, I came across an online ad for hearing aids at less than half the clinic price. The deal seemed too good to pass up — until I read the fine print. The devices weren’t FDA-regulated, and there was no professional fitting or follow-up support. I realized I’d be on my own if they didn’t work or caused discomfort. That’s when I understood a critical truth: hearing aids aren’t one-size-fits-all. They need to be programmed to your specific hearing profile, fitted to your ear anatomy, and adjusted over time as you adapt. Skipping the audiologist might save money today, but it risks poor performance, physical discomfort, and wasted spending tomorrow.

Another trap is delaying treatment to save cash. It’s tempting to wait, especially if hearing loss feels mild. But research shows that the longer you wait, the harder it is to adjust to hearing aids later. The brain adapts to silence, and relearning how to process sound takes longer when treatment is delayed. That means more follow-up visits, longer trial periods, and potentially higher overall costs. There’s also the risk of irreversible consequences — like accelerated cognitive decline or social withdrawal — that no device can fully reverse.

I also learned to be cautious about bundled pricing. Some clinics offer “free” hearing tests but then pressure patients into high-cost purchases. Others bundle accessories or extended warranties that may not be necessary. I made sure to ask for itemized pricing and to understand exactly what I was paying for. Transparency mattered. I wanted a provider who treated me as a long-term patient, not a one-time sale. In the end, I chose a clinic with a strong reputation, clear pricing, and a commitment to follow-up care. That decision cost more upfront, but it saved me from costly mistakes and frustration down the road.

Building a Health-First Investment Philosophy

Looking back, buying hearing aids wasn’t just a medical purchase — it was the start of a new way of thinking. I began applying the same logic to other areas of my health. I scheduled regular eye exams, invested in ergonomic furniture for my home office, and started prioritizing mental wellness through mindfulness and therapy. Each decision followed the same principle: treat your body and mind as valuable assets worth maintaining. When you’re healthier, you work better, think more clearly, and engage more fully with life — all of which support long-term financial well-being.

This health-first philosophy isn’t about spending more money — it’s about spending it wisely. It’s choosing prevention over crisis care, quality over bargain, and long-term value over short-term savings. It’s recognizing that your ability to earn, connect, and enjoy life depends on your physical and mental condition. And while no investment is risk-free, few offer the compounding returns of good health. The benefits ripple outward — stronger relationships, greater resilience, improved decision-making — creating a foundation for lasting stability.

Today, I no longer see hearing aids as a cost. I see them as a daily reminder that the most reliable asset I’ll ever own is myself. I hear my children’s laughter more clearly. I contribute more confidently at work. I feel present in my life. That’s not just priceless — it’s profitable in the deepest sense. If you’re hesitating to invest in your hearing, know this: you’re not just restoring sound. You’re protecting your future, your relationships, and your ability to thrive. And that’s a return worth every penny.