What I Wish I Knew Before Losing My Job: Avoiding Financial Traps

Losing a job doesn’t just hurt emotionally—it can wreck your finances fast if you’re not careful. I learned this the hard way. When my position was eliminated, panic kicked in. I made rushed moves, drained savings, and almost fell into serious debt. This is the real talk I needed back then: how to protect your money, avoid common pitfalls, and stay in control when income stops. No jargon—just practical steps from someone who’s been there. It’s not about having a perfect plan from day one; it’s about avoiding the most damaging mistakes that can set you back for years. The truth is, financial resilience isn’t built in a crisis—it’s built before it. But if you’re already in the middle of one, this guide can help you steady the ship and move forward with clarity and confidence.

The Emotional Money Spiral: Why Panic Is Your Biggest Risk

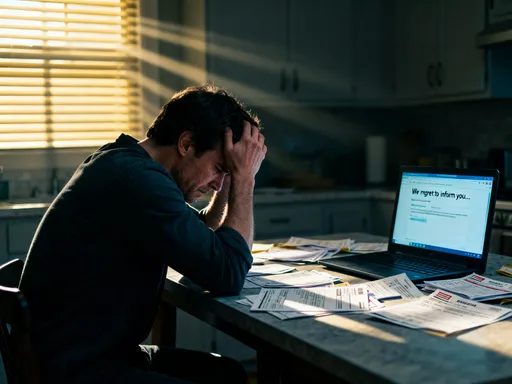

When the paycheck stops, fear takes over quickly. It’s natural to feel overwhelmed, anxious, and even ashamed when you lose your job. These emotions, while valid, can become dangerous when they drive your financial decisions. Many people react to job loss by either freezing completely—ignoring bills and statements—or swinging to the opposite extreme: making impulsive, high-stakes choices in an attempt to regain control. The emotional money spiral begins with stress and ends with long-term damage to your financial health.

One of the most common reactions is emotional spending. Some people treat themselves to a “last hurrah” dinner, a new piece of furniture, or an unplanned trip, telling themselves they “deserve it” after the stress of being let go. Others start buying comfort items—clothes, electronics, takeout meals—not out of need, but to soothe anxiety. This behavior mimics coping mechanisms seen in other stressful life events, and it can silently erode your financial cushion. On the flip side, some respond by cutting every non-essential expense overnight, including things like gym memberships, internet, or even basic maintenance on the car. While frugality is wise, over-cutting can backfire by making daily life harder and reducing your ability to stay active in the job search.

The real danger lies in irreversible decisions made under pressure. For example, withdrawing money from a retirement account like a 401(k) might seem like a quick solution, but it comes with steep penalties and tax consequences. The IRS typically charges a 10% early withdrawal penalty on distributions before age 59½, and the amount withdrawn is added to your taxable income for the year. That means a $20,000 withdrawal could result in nearly $7,000 in combined taxes and penalties, depending on your tax bracket. What feels like $20,000 in emergency funds becomes closer to $13,000 in usable cash—and you’ve permanently damaged your long-term savings trajectory.

The best defense against the emotional money spiral is a pause. Experts recommend waiting at least 72 hours before making any major financial move after job loss. Use that time to gather information: review your savings, calculate your monthly burn rate, and map out your unemployment benefits. Talk to a trusted friend or financial counselor, not to get emotional support alone, but to create accountability. Writing down your feelings can also help separate emotion from action. When you approach your finances with intention instead of instinct, you’re far more likely to make choices that protect your future rather than react to your present fear.

The False Safety of Over-Drawing Savings

Savings are meant to be a safety net, not a bottomless pit. Yet, when income vanishes, it’s easy to fall into the trap of treating your emergency fund like an endless resource. The psychological comfort of seeing a healthy balance can lead to careless withdrawals—just $500 here for groceries, $1,000 there for car repairs—without tracking the total impact. Over time, these withdrawals add up, and before you know it, the cushion you worked years to build is gone, leaving you exposed to further setbacks.

The problem isn’t using savings—it’s using them without a plan. A structured drawdown strategy is essential. Start by calculating your essential monthly expenses: housing, utilities, food, transportation, insurance, and minimum debt payments. These are non-negotiables. Once you have that number, divide your total emergency fund by it to determine how many months of coverage you have. For example, if you have $18,000 saved and your essential costs are $3,000 per month, you have six months of runway. That figure becomes your financial countdown clock.

From there, set a strict monthly withdrawal limit. Instead of dipping into savings as needed, transfer a fixed amount each month into your checking account, just as if it were a paycheck. This creates discipline and prevents overspending. If you have $18,000 and six months of coverage, withdraw $3,000 per month and no more. Any leftover funds at the end of the month can roll over, extending your timeline. This method transforms your savings from a reactive resource into a planned income substitute.

It’s also important to distinguish between essential and non-essential uses of savings. Paying the rent? Essential. Replacing a broken laptop needed for job applications? Essential. Eating out three times a week? Not essential. Upgrading your phone because the old one feels slow? Not essential. Creating clear categories helps you stay focused. Some people even open a separate bank account just for unemployment spending, transferring the monthly amount and leaving the rest untouched. This physical separation reduces temptation and reinforces discipline.

Remember, the goal isn’t to preserve every dollar at all costs—it’s to make your savings last long enough to find stable income. If you drain your fund in two months, you’ll face much tougher choices later. But if you stretch it to eight or nine months, you give yourself breathing room to make thoughtful decisions, not desperate ones.

Credit Cards: Lifeline or Quicksand?

Credit cards can feel like a financial lifeline when your income stops. With just a swipe, you can cover groceries, gas, and even rent. But unlike cash or savings, credit doesn’t solve the problem—it delays it, often at a steep cost. The real danger lies in the compounding interest and the illusion of affordability created by minimum payments. A balance that seems manageable today can balloon into a long-term burden, especially without a steady income to pay it down.

Consider this scenario: you charge $2,000 to your credit card to cover a month’s expenses. Your card has a 20% annual interest rate, and your minimum payment is $50. If you only pay the minimum each month, it will take over five years to pay off the balance, and you’ll end up paying more than $600 in interest—nearly a third of the original amount. That’s money you don’t have, earned by a bank, not you. And if you continue using the card, the cycle worsens. This is how credit becomes quicksand: easy to step into, hard to escape.

The key is to treat credit as a last resort, not a first option. If you must use a card, do so with a clear repayment plan. Decide in advance how you’ll pay it off—whether through future income, a side gig, or a specific savings allocation. Avoid using credit for recurring expenses like utilities or groceries unless absolutely necessary. These charges add up fast and are hard to eliminate once the habit forms.

If you’re already carrying a balance, look into alternatives that can reduce the cost. Balance transfer cards with 0% introductory rates can help you avoid interest for 12 to 18 months, giving you time to pay down debt without it growing. But read the fine print: after the introductory period, the rate jumps, and there’s often a 3% to 5% fee for the transfer. Another option is a hardship program offered by many credit card issuers. These programs may lower your interest rate, waive fees, or allow reduced payments for a set period. They don’t hurt your credit score and are designed for people facing job loss or medical issues. You just have to ask.

The bottom line: credit cards are tools, not solutions. Used wisely, they can help you bridge a short gap. Used recklessly, they can deepen your financial hole and delay recovery by years. The difference lies in intention, awareness, and control.

Skipping Insurance: A Risk That Backfires

When money is tight, insurance premiums can feel like an easy place to cut costs. Health, car, and even homeowners insurance require monthly payments that don’t offer immediate, visible returns. It’s tempting to think, “I’m healthy—I don’t need coverage,” or “I drive carefully—I’ll be fine without insurance.” But going uninsured is not a savings strategy; it’s a high-stakes gamble with potentially devastating financial consequences.

Health insurance is the most critical. A single emergency room visit can cost thousands of dollars. A hospital stay for pneumonia or a broken bone might run $10,000 to $30,000 or more, depending on treatment. Without insurance, you’re responsible for the full bill. Even if you negotiate with the hospital, the amount owed can still be unaffordable, leading to collections, damaged credit, and even lawsuits. Some people assume they can rely on Medicaid, but eligibility varies by state and income, and the application process can take weeks. In the meantime, one medical incident can wipe out savings and lead to long-term debt.

Car insurance is another area where people take dangerous risks. In most states, driving without insurance is illegal and can result in fines, license suspension, or even vehicle impoundment. If you cause an accident, you could be held personally liable for damages, medical bills, and legal fees—costs that can reach hundreds of thousands of dollars. Even if you’re not at fault, being uninsured can complicate claims and leave you without coverage for repairs or rental cars.

The good news is that there are ways to reduce insurance costs without canceling coverage. For health insurance, you may qualify for COBRA, which allows you to keep your employer’s plan for up to 18 months. While expensive—since you pay the full premium plus a small administrative fee—it ensures continuity of care. Alternatively, you can explore plans through the Health Insurance Marketplace, where subsidies based on income can significantly lower monthly costs. Some states also offer low-cost or free programs for unemployed residents.

For car insurance, contact your provider and explain your situation. Many companies offer reduced rates for unemployed drivers or allow you to adjust coverage temporarily—such as dropping collision on an older vehicle. But never cancel entirely. The short-term savings are never worth the long-term risk. Insurance is not an expense; it’s protection. And protection is what keeps a financial setback from becoming a financial disaster.

The Investment Temptation: Chasing Quick Returns

When income disappears, the urge to “make it up fast” can be overwhelming. Some people turn to their investment accounts, hoping to time the market or chase high returns through speculative trades. Others consider pulling money from retirement funds to start a business or invest in cryptocurrency, believing they can turn a small amount into a fortune. These moves are driven by desperation, not strategy, and they rarely end well.

Market timing—trying to buy low and sell high based on predictions—is notoriously difficult, even for professional investors. Studies show that most individuals who attempt to time the market underperform those who stay invested consistently. When you sell during a downturn, you lock in losses. When you buy during a rally, you risk buying high just before a correction. Emotional investing magnifies these mistakes. Fear leads to selling low; greed leads to buying high. The result is often a permanent reduction in portfolio value.

Withdrawing from retirement accounts like a 401(k) or IRA to fund short-term needs is another common but costly mistake. As mentioned earlier, early withdrawals trigger taxes and penalties. But beyond the immediate cost, you lose the power of compound growth. That $10,000 you take out today could have grown to over $60,000 in 20 years, assuming a 7% annual return. By spending it now, you’re not just losing $10,000—you’re losing decades of future growth.

Instead of raiding investments, focus on preserving them. Keep contributing if possible, even in small amounts. If you’re unable to contribute, at least avoid selling. Review your asset allocation to ensure it’s still appropriate for your age and risk tolerance, but don’t make drastic changes based on short-term emotions. Remember, investments are for the long term. A job loss is a temporary setback, not a reason to abandon your financial future.

If you’re considering starting a side business or investing in a new opportunity, do so with caution. Use only non-retirement funds, and limit your risk to what you can afford to lose. A small, calculated investment can pay off; a desperate gamble usually does not. Patience and discipline are your greatest allies in wealth building. They may not feel exciting, but they are reliable.

Ignoring Income Alternatives: The Hidden Opportunities

After losing a job, many people focus solely on finding a full-time replacement. While that should be the ultimate goal, waiting for the perfect offer can leave you financially vulnerable in the meantime. The truth is, there are many ways to generate income, even during a career transition. Ignoring these opportunities increases the pressure to make poor financial decisions, while embracing them can provide stability, confidence, and momentum.

Side gigs and freelance work are among the most accessible options. If you have skills in writing, editing, bookkeeping, graphic design, or virtual assistance, you can find short-term projects on platforms like Upwork or Fiverr. Even if the pay is modest, a few hundred dollars a month can cover groceries or a credit card bill, reducing the need to dip into savings. Teaching, tutoring, or offering consulting in your field are also viable paths. Many professionals have successfully turned years of experience into paid advice, workshops, or online courses.

Other options include seasonal work, delivery driving, pet sitting, or selling unused items online. These may not align with your long-term career, but they serve a purpose: keeping cash flowing. The psychological benefit is just as important as the financial one. Earning even a small amount reinforces a sense of agency and progress, counteracting the helplessness that often follows job loss.

The key is to view these efforts not as failures, but as strategic moves. They buy you time, reduce financial stress, and allow you to be more selective in your job search. You don’t have to accept the first offer that comes along if you have some income coming in. You can wait for a role that fits your skills and goals. This flexibility is a form of power—one that comes from planning, not luck.

Building a Resilient Mindset: From Survival to Strategy

Financial recovery begins in the mind. After job loss, it’s easy to fall into a survival mindset—focused only on making it through the next week or month. But long-term stability requires a shift to strategic thinking. This doesn’t mean ignoring stress or pretending everything is fine. It means acknowledging the challenge while taking deliberate, informed steps forward.

Start by setting small, achievable goals. Instead of saying, “I need a job,” break it down: “I will apply to three jobs this week,” or “I will update my resume by Friday.” Track your progress in a journal or planner. Each completed task builds confidence and momentum. Celebrate small wins—getting a response from a recruiter, completing a freelance project, sticking to your budget for a full month. These moments matter.

Reconnect with your values. Ask yourself: What kind of life do I want to build? What financial habits support that vision? This reflection helps you avoid making choices based solely on fear or urgency. It brings clarity to your decisions. Maybe you realize you don’t need a high-paying job in a field you dislike. Maybe you see an opportunity to pivot to something more fulfilling, even if it pays less at first. A resilient mindset allows for reinvention, not just recovery.

Finally, remember that financial setbacks don’t define your worth. Millions of people have lost jobs through no fault of their own. What matters is how you respond. Avoiding the common traps—emotional spending, credit overuse, insurance lapses, investment panic—puts you ahead of the curve. You’re not just surviving; you’re learning, adapting, and building strength for the future. The choices you make now won’t just get you through this moment—they’ll shape the foundation of your next chapter.