How I Nailed Tax Compliance While Crushing My Financial Goals

Let’s be real—taxes used to stress me out every year. I’d scramble last minute, overpay, or miss deductions that could’ve saved me serious cash. But after a few painful lessons, I figured out how to stay compliant *and* hit my financial targets without the panic. It’s not about being a genius—it’s about smart, simple habits. Here’s how I turned tax season from a nightmare into a power move for my finances.

The Wake-Up Call: When Tax Mistakes Cost Me More Than Money

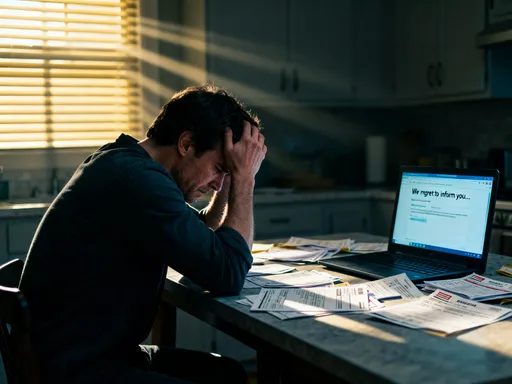

Tax season used to be a source of dread, not opportunity. For years, I treated filing as a one-time event—something to rush through in April with a mix of anxiety and coffee. I’d gather what little paperwork I had, use a basic online tool, and submit without a second thought. I believed as long as I paid something, I was in the clear. But one year, that mindset backfired in a big way. A minor error on a home office deduction—claiming square footage I didn’t properly document—triggered a notice from the IRS. What started as a routine inquiry spiraled into a full audit. The process took months. I had to produce bank statements, utility bills, lease agreements, and proof of business use. The stress was overwhelming. I lost sleep, missed work hours, and paid hundreds in late fees and interest, even though the original discrepancy was small. More than the money, it was the loss of control that stung. I realized then that tax compliance isn’t a side task—it’s central to financial stability. One oversight, no matter how small, can disrupt savings plans, delay home purchases, or derail retirement goals. That experience was my wake-up call. I decided I would never again treat taxes as an afterthought. Instead, I began to see them as a critical part of my financial health, just like budgeting or saving for emergencies. From that point on, I committed to understanding the rules, keeping better records, and building systems that ensured I stayed on the right side of compliance—not just to avoid penalties, but to protect everything I was working toward.

Linking Taxes to Financial Goals: Why Compliance Fuels Growth

Once I shifted my perspective, I began to see taxes not as a burden, but as a strategic lever in my financial life. Every dollar I overpay in taxes is a dollar that isn’t compounding in my retirement account, paying down debt, or funding a family vacation. When I stay compliant, I don’t just avoid fines—I position myself to grow wealth more effectively. For example, knowing the rules around retirement contributions allows me to maximize my 401(k) and IRA limits each year. That reduces my taxable income now and builds long-term savings. Similarly, understanding how capital gains are taxed helps me decide when to sell investments, ensuring I keep more of my profits. Compliance also opens doors to credits and deductions that directly support my goals. The Child Tax Credit, for instance, put hundreds of dollars back in my pocket each year—money I redirected toward college savings. The Earned Income Tax Credit boosted my refund when I was building my side business, giving me extra capital to reinvest. These aren’t loopholes; they’re incentives built into the tax code to reward certain behaviors like saving, education, and home ownership. When I align my actions with these incentives, I’m not just following the law—I’m using it to my advantage. I also found that clean, accurate records make financial planning easier. When tax time rolls around, I already have a clear picture of my income and expenses, which helps me adjust budgets, forecast cash flow, and make smarter investment decisions. In short, tax compliance isn’t separate from financial success—it’s a core component. It provides the structure and clarity needed to move forward with confidence, knowing I’m not carrying hidden risks or leaving money on the table.

Smart Record-Keeping: The Quiet Game-Changer

One of the most transformative changes I made was overhauling how I manage financial records. In the past, I kept receipts in a shoebox, mixed personal and business expenses, and rarely reviewed them until April. It was chaotic and inefficient. Now, I track everything digitally from day one. I use a cloud-based accounting app that syncs with my bank accounts and credit cards, automatically categorizing transactions. Every time I make a purchase, whether it’s office supplies or a business meal, I take a photo of the receipt and upload it to the system. This might sound like overkill, but the payoff has been enormous. During one tax season, I discovered I’d overlooked nearly $1,200 in deductible expenses—things like software subscriptions, professional development courses, and mileage for client meetings. These weren’t exotic deductions; they were ordinary costs I simply hadn’t tracked properly. Beyond the direct savings, this habit gave me a much clearer understanding of where my money goes. I started noticing patterns: certain subscriptions I no longer used, recurring expenses that could be negotiated, and opportunities to shift spending to more tax-advantaged categories. I also feel more confident knowing my records are organized and accessible. If the IRS ever questions a deduction, I can pull up documentation in seconds. This peace of mind is priceless. Digital tools have made this process easier than ever. Many apps offer features like automatic mileage tracking, receipt scanning, and integration with tax preparation software. Some even flag potential deductions based on spending patterns. I don’t spend hours on this—just a few minutes each week to review and categorize. The key is consistency. By making record-keeping a routine part of my financial life, I’ve turned a once-dreaded task into a quiet source of power. It’s no longer about surviving audit season; it’s about building a foundation of clarity and control that supports every financial decision I make.

Timing Matters: When to Pay, When to Defer, and Why

Another insight that changed my approach was learning how timing affects tax outcomes. Not all income and expenses are treated the same, and when you recognize that, you gain a surprising amount of control. For instance, I run a small consulting business, and my income varies from month to month. I learned that I can legally delay invoicing a client until January, pushing that income into the next tax year. That might not sound like much, but if I’m close to a higher tax bracket, deferring even a few thousand dollars can keep me in a lower rate. On the flip side, I can accelerate certain deductible expenses—like paying for a professional conference or upgrading my computer—before December 31. That reduces my taxable income for the current year. This isn’t about hiding money; it’s about using the tax code as it’s intended. The same principle applies to retirement accounts. If I’ve under-contributed to my IRA, I can make a lump-sum deposit by the April filing deadline and still count it for the previous year. That’s a powerful way to lower my tax bill while boosting long-term savings. I also pay attention to how different types of income are taxed. For example, long-term capital gains have lower rates than ordinary income, so I plan my investment sales accordingly. I don’t time the market, but I do consider the tax implications of each sale. These strategies don’t require complex schemes or risky moves—they’re simple, legal decisions that add up over time. The result? More breathing room in my budget, more money to reinvest, and fewer surprises when tax season arrives. I now treat December as a strategic planning month, not just a holiday rush. I review my income, projected tax liability, and deductible expenses to see if any adjustments make sense. This proactive approach has saved me hundreds, sometimes thousands, each year. It’s not about gaming the system—it’s about working with it wisely, so my money works harder for me.

Deductions and Credits: The Hidden Tools in Plain Sight

One of the biggest mistakes I made early on was assuming I didn’t qualify for deductions or credits. I thought they were only for big businesses or high earners. But the truth is, many are designed for everyday people—parents, students, homeowners, and small business owners like me. I missed out for years simply because I didn’t know what was available. The turning point came when I discovered the Lifetime Learning Credit. I was taking an online course to expand my skills, and I had no idea the tuition could qualify for a tax credit of up to $2,000. That single credit cut my tax bill significantly. Another win was the home office deduction. Once I started tracking my space and usage correctly, I was able to claim a portion of my rent, utilities, and internet—adding up to hundreds in savings. These aren’t secret tricks; they’re part of the tax code, waiting to be used. The key is knowing what applies to your specific situation. For example, if you’ve made energy-efficient upgrades to your home—like installing solar panels or energy-saving windows—you may qualify for the Residential Clean Energy Credit. If you’re paying off student loans, you might be eligible for the student loan interest deduction, which allows you to deduct up to $2,500 in interest paid each year. Even transportation choices can matter: using a commuter benefit or taking advantage of employer-sponsored transit programs can reduce taxable income. I now make it a habit to review potential deductions and credits every quarter, not just in April. I keep a running list and update it as my life changes—new expenses, new dependents, new goals. This ongoing awareness has turned tax planning into a year-round practice. I don’t wait for tax season to find savings; I build them into my routine. And because I stay informed, I can make smarter financial decisions throughout the year, knowing how each choice might affect my tax picture. These tools aren’t about getting something for nothing—they’re about getting what you’re already entitled to, so you can keep more of what you earn.

Working with Pros: When DIY Isn’t Worth the Risk

For a long time, I prided myself on doing everything myself—budgeting, investing, even tax filing. I used online software and thought I had it covered. But as my financial life grew more complex—multiple income streams, self-employment, investments, and a growing family—I hit a wall. The rules changed, new credits were introduced, and I realized I didn’t have the time or expertise to stay on top of it all. That’s when I decided to hire a certified tax professional. It felt like an added expense at first—around $400 for a full return—but it paid for itself within the first year. My tax preparer identified deductions I had no idea existed, including a qualified business income deduction that saved me over $600. They also ensured my records were audit-ready, advised me on retirement contributions, and helped me set up a system for quarterly estimated taxes. Most importantly, they gave me confidence. I no longer worry about making a costly mistake. I still manage my day-to-day finances, track expenses, and keep records—but I leave the final filing and strategy to someone with specialized knowledge. This isn’t a sign of failure; it’s a sign of smart resource management. Just like I wouldn’t try to fix my own car engine or diagnose a medical issue, I don’t expect myself to master every detail of tax law. A professional brings experience, up-to-date knowledge, and an objective eye. They can spot red flags before they become problems and suggest strategies I might never have considered. I now view this cost as a form of financial insurance. A small annual fee protects me from much larger potential losses. I also schedule an annual meeting with my tax advisor, not just during filing season. We review my goals, income changes, and life events to ensure my tax strategy stays aligned with my overall plan. This proactive partnership has made a measurable difference in my financial outcomes—and my peace of mind.

Building a Tax-Smart Mindset for Long-Term Wins

Today, tax compliance is no longer a source of stress—it’s a cornerstone of my financial strategy. I’ve built a rhythm that keeps me prepared all year long. Every quarter, I review my income, expenses, and tax withholdings. I adjust retirement contributions, track deductible purchases, and update my records. This consistent attention means I never face a last-minute scramble. Instead, tax season has become a moment of clarity—a chance to assess my progress, celebrate savings, and plan for the year ahead. This mindset shift didn’t happen overnight. It took time, a few mistakes, and a willingness to learn. But the rewards have been worth it. I’m not just avoiding penalties—I’m unlocking opportunities. I’ve redirected thousands of dollars from overpayments into savings, investments, and family goals. I feel more in control of my money and more confident in my decisions. The biggest lesson I’ve learned is that compliance isn’t the enemy of financial freedom—it’s a prerequisite. When your taxes are handled with care, your entire financial life becomes more stable, predictable, and powerful. You’re not just surviving the system; you’re using it to build something lasting. Whether you’re a parent managing a household budget, a freelancer building a business, or someone saving for retirement, the principles are the same: stay informed, keep good records, use available tools, and don’t hesitate to get help when needed. Tax compliance isn’t a burden to endure—it’s a foundation to build on. And when you get it right, it doesn’t just protect your past; it empowers your future.